- Slowdown in productivity growth posing a medium term challenge for developing countries

- Weaker-than-expected first quarter growth in the United States of America

- Plunge in cocoa prices delaying economic recovery in West Africa

GLOBAL ISSUES

RECENT SLOWDOWN IN PRODUCTIVITY GROWTH HIGHLIGHTS MEDIUM-TERM CHALLENGES FOR DEVELOPING COUNTRIES

Recent indicators have shown a gradual strengthening of global economic activity since late 2016. In tandem with an improvement in aggregate demand, international trade and manufacturing output have rebounded, while commodity prices have risen from their lows seen in early 2016. Amid a general improvement in business sentiment, several large economies, including the United States of America and Japan, are experiencing a moderate recovery in investment. Against a backdrop of elevated uncertainty and downside risks, however, it is still unclear whether this positive global growth momentum can be sustained going forward. Several lingering structural weaknesses are also constraining the medium-term growth outlook. Of particular concern is the prolonged and broad-based weakness in global productivity growth since the global financial crisis.

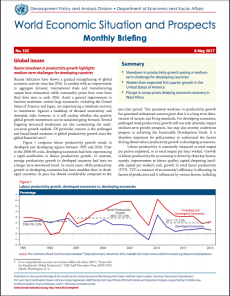

![Figure 1: Labour productivity growth, developed economies vs. developing economies]()

Figure 1 compares labour productivity growth trends in developed and developing regions between 1995 and 2016. Prior to the 2008-09 crisis, developing economies had been experiencing a rapid acceleration in labour productivity growth. In contrast, average productivity growth in developed countries had been on a longer term downward trend. In recent years, while productivity growth in developing economies has been steadfast than in developed countries, its pace has slowed considerably compared to the pre-crisis period. This persistent weakness in productivity growth has generated widespread concern given that it is a long-term determinant of income and living standards. For developing economies, prolonged weak productivity growth will not only adversely impact medium-term growth prospects, but may also severely undermine progress in achieving the Sustainable Development Goals. It is therefore important for policymakers to understand the factors driving slower labour productivity growth in developing economies.

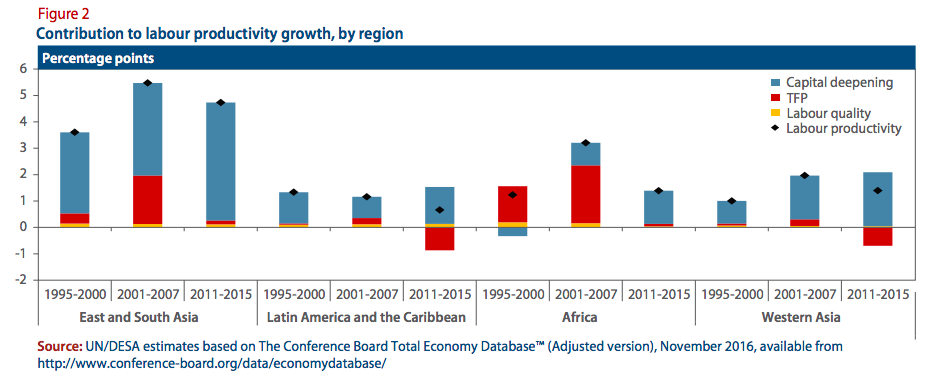

Labour productivity is commonly measured as total output per person employed, or as total output per hour worked. Growth in labour productivity for an economy is driven by three key factors, namely, improvements to labour quality; capital deepening (available capital per worker); and, growth in total factor productivity (TFP). TFP is a measure of an economy’s efficiency in allocating its factors of production and is influenced by various factors, including economies, the slowdown in labour productivity growth has been largely attributed to the decline in the contribution from capital formation. This reflects the persistent weakness in investment growth in these economies since the financial crisis, as capital spending remains constrained by sluggish demand, high uncertainty and fragile bank balance sheets.

Across many developing regions, however, capital deepening has continued to contribute positively to labour productivity growth, implying that investment in new capital has held up relatively well in the post-crisis period (figure 2). Instead, the recent slowdown in labour productivity growth in developing countries has been mainly due to a deceleration in TFP growth. is suggests that developing countries are, on average, experiencing slower efficiency gains and technological absorption following the recession.

![Figure 2: Contribution to labour productivity growth, by region]()

Several cyclical and structural factors appear to have contributed to the broad-based slowdown of TFP growth in developing economies. On the cyclical front, subdued demand conditions—amid high uncertainty in the post-crisis environment—may have affected the quality of investment, resulting in lower TFP growth. In addition, recent evidence has shown that TFP growth in the commodity-exporting economies tends to move in tandem with commodity prices, given that commodity-related income facilitates investment in technology and human capital. Hence, the end of the super-cycle of commodity prices in recent years has contributed to the slowdown in productivity growth in several regions, including in Africa, Latin America and Western Asia.

Beyond these cyclical factors, several structural shifts had also taken place, notably the waning effects of past advances that catalysed strong TFP growth in the last two decades. First, the surge of information and communication technology in the 1990s contributed to improved productivity in the global economy, including in developing economies. Second, earlier structural reforms and transformation processes spurred large productivity gains in several countries. For instance, China’s transition from an agrarian economy to an industrial powerhouse was accompanied by rapid technological progress and increased workforce efficiency. Third, major trade liberalization efforts, such as the formation of the European Union and China’s accession into the World Trade Organization, drove rapid growth in international trade in the 2000s. This development could have stimulated TFP growth in many developing economies, given that trade increases competition and drives the distribution of new technology. In particular, the proliferation of global value chains, for example in East Asia, not only generated large economies of scale, but also allowed for exporting firms to acquire new production techniques.

It is also important to highlight that a country’s potential to achieve stronger productivity growth is also influenced by its economic structure. Countries with a high dependency on natural resources face larger constraints to productivity growth, compared to countries where high technology manufacturing activities are more prevalent. In general, developing regions like Latin America or Western Asia have had limited success in promoting a process of structural change towards more technologically advanced sectors, thus restraining productivity gains through technical progress and innovation.

In the medium term, policy efforts in developing countries need to be geared towards reversing the current trends in productivity growth to enhance economic resilience and sustain growth prospects. Further progress needs to be made on structural reforms that can boost TFP growth. This includes strengthening governance, improving the quality of education and promoting initiatives to enhance innovation as well as investment in research and development.

DEVELOPED ECONOMIES

UNITED STATES: DISAPPOINTING START TO 2017

Gross domestic product (GDP) growth in the United States was on the downside in the first quarter of 2017, with the advance estimate showing growth of just 0.7 per cent on an annualized basis. While consumer confidence indicators rose following the elections in November 2016 and remain high today, this has not yet translated into stronger household spending. Personal consumption expenditure showed negligible growth in the first quarter of the year, with a sharp decline in spending on durable goods. A downward adjustment to the level of private inventories also contributed to the economic slowdown, reducing GDP growth by 0.9 percentage points. There is a risk that the weaker-than-expected GDP growth may lead to a reversal of the upbeat economic sentiment and buoyant stock market performance in the United States, putting the Government’s target of achieving annual GDP growth of 3 to 4 per cent further from reach.

The Federal Open Market Committee (FOMC) of the United States Federal Reserve kept interest rates unchanged at its meeting in May. While financial markets continue to expect a 25 basis points rise in interest rates in the United States at the next monetary policy meeting in June, the FOMC may move more slowly if confidence indicators deteriorate or if signs of an acceleration in real economic activity fail to emerge.

JAPAN: UNEMPLOYMENT RATE AT 22-YEAR LOW

The unemployment rate in Japan dropped to 2.8 per cent in February and remained stable in March, the lowest level recorded since 1994. At the same time, the Tankan factor utilization index stands at its highest level since 1990 and the Bank of Japan’s (BoJ) estimate of the output gap is positive, showing positive gaps in both labour and capital inputs. The BoJ is committed to maintaining its policy of “Quantitative and Qualitative Monetary Easing with Yield Curve Control”, aiming to achieve the price stability target of 2 per cent. Nonetheless, wage pressures remain moderate and inflation is unlikely to reach the central bank target this year or next. Nationwide consumer price inflation averaged -0.1 per cent in 2016, but has been positive in the first months of 2017, hovering close to zero. The uptick in inflation, which reached 0.2 per cent in March, primarily reflects higher energy prices and the depreciation of the yen in late 2016.

EUROPE: SLOWER INFLATION AND SOLID GAINS IN NOMINAL WAGES

In March, inflation in the European Union slowed to 1.6 per cent from 2.0 per cent in the previous month, due mainly to a slower increase in energy prices. Romania, with 0.4 per cent, and Ireland and the Netherlands, both with 0.6 per cent, registered the lowest inflation rates in the region, while Latvia and Lithuania experienced the fastest price increases, at 3.3 per cent and 3.2 per cent, respectively. At the same time, nominal wages showed solid gains in several countries. In Germany, nominal wage growth in industry reached 3.0 per cent in February, which translated into some gains in real purchasing power due to the moderate level of inflation. Similarly, in Poland, the average wage level increased by 5.2 per cent in March, although one o payments underpinned part of this increase. In both cases, these trends will further drive private consumption, which has been playing an important role for the overall growth performance.

As inflation in the Czech Republic was unexpectedly on the upside in March, reaching 2.6 per cent, in early April the Czech National Bank concluded its policy of maintaining a ceiling on the value of the koruna, which was initiated in late 2013 as an additional monetary policy tool.

ECONOMIES IN TRANSITION

In the first quarter, macroeconomic indicators in the Commonwealth of Independent States (CIS) area show a heterogeneous growth performance. In Central Asia, Kyrgyzstan recorded strong GDP growth of 7.8 per cent as gold production increased, while a recovery in remittances from the Russian Federation bolstered household income. In the Caucasus, the economic activity indicator strengthened by 6.6 per cent in Armenia. Among the CIS energy-exporters, the implementation of development programmes contributed to 3 per cent growth in Kazakhstan. In contrast, the Azerbaijan economy shrunk by 0.9 per cent, largely due to a drastic decline in oil output. This was attributed in part to the commitment to production cuts as agreed by Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC members at the end of 2016.

Inflationary trends in the region also diverged. Armenia saw a 0.9 per cent deflation in the first quarter. In Azerbaijan, however, inflation accelerated to 14.5 per cent in March, driven by higher food prices. Inflation also increased in Ukraine to 15.1 per cent, due to higher production costs.

In the Russian Federation, inflation is contained at slightly over 4 per cent, in part held back by subdued domestic demand, but also the strong rouble bringing down import prices and inflationary expectations. In late April, the central bank further reduced its policy rate by 50 basis points to 9.25 per cent. Due to still high real interest rate, however, this move will impact carry trade and the exchange rate only moderately. Policy rates were also reduced in Belarus, where inflation subsided considerably alongside an appreciation of the domestic currency, and in Ukraine.

In South-Eastern Europe, the Albanian economy expanded by over 3.4 per cent in 2016. Robust export performance significantly contributed to growth in the fourth quarter. The country has absorbed about €1 billion of foreign investments in 2016.

DEVELOPING ECONOMIES

AFRICA: PLUMMETING COCOA PRICES HIT WEST AFRICAN ECONOMIES

Plummeting prices are hurting the finances of cocoa producing countries and incomes for hundreds of thousands of small-scale farmers. Cocoa prices have plunged by over 40 per cent since last year, hitting a 10-year low, as a result of bumper crops and stagnant demand around the world. Cocoa is the main produce of Côte d’Ivoire and accounts for about a fifth of the nation’s exports. It is also among the main exports of Cameroon, Ghana, Guinea, Nigeria, São Tomé e Príncipe and Sierra Leone.

In Cameroon, the price decline is affecting 600,000 households whose livelihoods are derived from cocoa. Ghana, the second largest world producer of cocoa, has lost almost $1 billion in export revenue. Côte d’Ivoire, the world’s top cocoa exporter, announced that it would reduce its 2017 budget by one tenth, although the move was also triggered by wage demands from civil servants and soldiers. The decision follows a recent one to cut prices paid to farmers by 36 per cent, as a disincentive to raise output. In the coming months, the World Bank will grant the country $100 million to $125 million in budget support. Cocoa-growing countries plan to fight the price rout by coordinating production strategies and promoting local consumption of chocolate.

There is, however, room for some optimism. Though a production surplus is likely to last through this year, the price weakness is not uncharacteristic of the market, which has seen considerable historical volatility. Most importantly, there is potential for growth in world cocoa consumption, given the possible demand growth in developing markets over the long term.

EAST ASIA: FIRST QUARTER GROWTH EXCEEDS EXPECTATIONS

Amid an improvement in domestic demand and a recovery in exports, a few major East Asian countries experienced faster-than-expected growth in the first quarter of 2017. In China, GDP growth picked up slightly to 6.9 per cent on a year-on-year basis. The industrial sector expanded at a stronger pace, driven in part by government stimulus measures and continued rapid credit growth. In the tertiary sector, services such as accommodation, real estate, retail and finance grew at a faster pace. However, these improvements were more than offset by a deceleration in transport and other services. From a demand perspective, private consumption remained the largest contributor to GDP growth, supported by a rise in disposable income and stronger job creation. Growth in fixed asset investment also accelerated, driven mainly by infrastructure and real estate investment.

Despite high political uncertainty, the economy of the Republic of Korea expanded at a faster pace of 2.7 per cent in the first quarter. Exports rebounded during the quarter, bolstered by an increase in shipments of semiconductors and machinery and equipment. Growth was also supported by stronger investment in facilities and sustained private consumption. Similarly, Taiwan Province of China also grew at a faster-than-expected pace of 2.6 per cent, driven mainly by higher exports of electronics. In addition, the recent announcement of a $29 billion (5.2 per cent of GDP) stimulus package, spread over 8 years, will provide a boost to domestic demand going forward.

SOUTH ASIA: PAKISTAN’S EXTERNAL SECTOR DETERIORATES VISIBLY, UNDERSCORING MEDIUM-TERM CHALLENGES

Since early 2016, the external sector has visibly deteriorated in Pakistan, owing to largely stagnant exports and a significant rise in imports. In the nine months to March 2017, the trade deficit increased by 28 per cent year-on-year to a record high of $19.7 billion, with the monthly import bill surpassing $5.0 billion for the first time in March. In particular, export growth has been restrained by relatively subdued external demand, growing competition in the garment sector from other Asian economies, and structural constraints, including power shortages. Meanwhile, imports of goods have increased markedly due to the implementation of large infrastructure projects, including the Pakistan-China Economic Corridor. As a result, the current account deficit has widened considerably, while international reserves declined from almost $19 billion in October 2016 to $17.1 billion in February 2017. These developments have prompted the Government of Pakistan to seek additional foreign loans from multilateral institutions and Chinese State-owned banks. In the short-term, the Pakistan economy is expected to navigate these external headwinds, amid solid private consumption and investment demand. In the medium term, however, strengthening the competitiveness of exports in Pakistan is a key challenge in order to reduce its external fragilities and to achieve a stronger, more balanced and sustainable growth.

WESTERN ASIA: RISING UNEMPLOYMENT

Unemployment rates are climbing in Western Asia, except for Israel where the unemployment rate remains at a historically low level. The Turkish unemployment rate reached 13 per cent in January 2017, the highest since February 2010. The unemployment rate among the Saudi nationals, excluding foreign labour, stood at 12.3 per cent in the fourth quarter of 2016, the highest since the first half of 2012. The unemployment rate of Jordan remained at 15.8 per cent in the fourth quarter of 2016, the highest since 2003. The large number of settled Syrian refugees and evacuees has pushed up the unemployment rate in Jordan and Turkey, where employment creation has also been held back by stagnated growth. For Saudi Arabia, a surge in the female unemployment rate is a dominant factor behind rising unemployment. While the male Saudi unemployment rate stood at 5.3 per cent in the fourth quarter of 2016, the female Saudi unemployment rate stood at 34.5 per cent. This partly reflects the rising female labour participation rate in recent years, from 12.6 per cent in 2006 to 19.3 per cent in the fourth quarter of 2016.

LATIN AMERICA AND THE CARIBBEAN: PROLONGED ECONOMIC CONTRACTION HAS ADVERSELY IMPACTED THE REGION’S LABOUR MARKET

Two years of economic contraction in Latin America and the Caribbean have had a pronounced impact on the region’s labour market. The average urban employment rate has declined steadily since early 2014 as economic activity in South America weakened substantially. At the same time, the quality of employment, as measured for example by the share of vulnerable employment, has worsened. Average unemployment in the region is estimated to have risen from 7 per cent in 2014 to 9 per cent in 2016 with a further increase projected for 2017. Brazil’s labour market has been hit particularly hard, with unemployment rising from a low of 6.2 per cent in late 2013 to 13.2 per cent by February 2017. In parallel, Brazil’s employment-to-population ratio has fallen to the lowest level since the series began in 2012. Most other South American economies have also seen unemployment increase over the past two years, albeit at a much lower rate. Recent labour market trends in Mexico and Central America have generally been more favourable although the subregion continues to face significant structural problems. Mexico’s unemployment rate fell to 3.2 per cent in March 2017, the lowest level in almost a decade. The incidence of informal work has also declined, but remains high at 57 per cent of total employment.

Institut français India proudly announces

Institut français India proudly announces

Interested

Interested

Pop star Ariana Grande today suspended her tour until early June at the earliest after a deadly attack on her show in Manchester that left 22 people dead.

Pop star Ariana Grande today suspended her tour until early June at the earliest after a deadly attack on her show in Manchester that left 22 people dead.

US President Donald Trump arrived at the Vatican on Wednesday for talks with one of his most high-profile critics, Pope Francis, after the two men exchanged sharp words during the presidential campaign last year.

US President Donald Trump arrived at the Vatican on Wednesday for talks with one of his most high-profile critics, Pope Francis, after the two men exchanged sharp words during the presidential campaign last year.

· India will grow at 7.2% in 2017-18, says World Bank – World Bank expects India , the fastest growing major economy in the world, to grow at 7.2% in the current fiscal and further up to 7.7 % by 2019-20 on strong fundamentals, reform momentum and improving investment scenario. Economic activity ought to accelerate in 2017-18.

· India will grow at 7.2% in 2017-18, says World Bank – World Bank expects India , the fastest growing major economy in the world, to grow at 7.2% in the current fiscal and further up to 7.7 % by 2019-20 on strong fundamentals, reform momentum and improving investment scenario. Economic activity ought to accelerate in 2017-18.

The 2017 MBDA-ISAE-French Embassy scholarship winners were felicitated at a ceremony held at the Residence of France on June, 01, 2017. Deputy Chief of Mission, Claire Thuaudet and Loïc Piedevache, MBDA India Country Head presented the scholarship certificates to the winners.

The 2017 MBDA-ISAE-French Embassy scholarship winners were felicitated at a ceremony held at the Residence of France on June, 01, 2017. Deputy Chief of Mission, Claire Thuaudet and Loïc Piedevache, MBDA India Country Head presented the scholarship certificates to the winners.

” It was an honour for FISME to organize the first India Commonwealth SME Trade Summit in New Delhi. Welcoming the policy makers and delegates from scores of Commonwealth nations, I tried to attract their attention towards Trade Facilitation. It is an issue of critical importance for SMEs. Today, the biggest challenges that SMEs face while exporting are in the realm of non-tariff. The unavailability of relevant information required for clearance of goods, opaque procedures, technical standards and lack of MRAs among labs frustrates SMEs’ efforts for accessing new markets. While in many countries, institutional arrangements have been put in place following WTO Trade Facilitation Agreement, it continues to be an uphill task for SME exporters to leverage them for ironing out market access barriers in importing countries. FISME strongly advocated how the private sector led arrangement of cooperation could be facilitated to smooth market access and facilitate trade. The participating policy makers and SMEs discussed, debated and agreed upon a Framework of MSME Cooperation covering most of the issues we raised. The framework was adopted as declaration as the outcome of Summit. It was heartening for me personally and professionally to be part of the facilitative process. ”

” It was an honour for FISME to organize the first India Commonwealth SME Trade Summit in New Delhi. Welcoming the policy makers and delegates from scores of Commonwealth nations, I tried to attract their attention towards Trade Facilitation. It is an issue of critical importance for SMEs. Today, the biggest challenges that SMEs face while exporting are in the realm of non-tariff. The unavailability of relevant information required for clearance of goods, opaque procedures, technical standards and lack of MRAs among labs frustrates SMEs’ efforts for accessing new markets. While in many countries, institutional arrangements have been put in place following WTO Trade Facilitation Agreement, it continues to be an uphill task for SME exporters to leverage them for ironing out market access barriers in importing countries. FISME strongly advocated how the private sector led arrangement of cooperation could be facilitated to smooth market access and facilitate trade. The participating policy makers and SMEs discussed, debated and agreed upon a Framework of MSME Cooperation covering most of the issues we raised. The framework was adopted as declaration as the outcome of Summit. It was heartening for me personally and professionally to be part of the facilitative process. ”")

Commerce Secretary for Government of India Ms. Rita Teaotia and Deputy Secretary General of Commonwealth Mr. Deodat Maharaj jointly inaugurated the first India Commonwealth SME Trade Summit on 30th June 2017 in New Delhi. Secretary MSME Dr. K.K. Jalan presided over the concluding session wherein the Framework of MSME Cooperation was adopted.

Commerce Secretary for Government of India Ms. Rita Teaotia and Deputy Secretary General of Commonwealth Mr. Deodat Maharaj jointly inaugurated the first India Commonwealth SME Trade Summit on 30th June 2017 in New Delhi. Secretary MSME Dr. K.K. Jalan presided over the concluding session wherein the Framework of MSME Cooperation was adopted.  The Summit was jointly supported by Department of Commerce, Ministry of Commerce and industries, Government of India and the Commonwealth secretariat (London), Over 400 delegates from over 25 countries participated in the Trade Summit including senior officials from Commonwealth countries. Besides the highly sought after Business-to-Business meetings, three concurrent Forums were also held during the Summit.

The Summit was jointly supported by Department of Commerce, Ministry of Commerce and industries, Government of India and the Commonwealth secretariat (London), Over 400 delegates from over 25 countries participated in the Trade Summit including senior officials from Commonwealth countries. Besides the highly sought after Business-to-Business meetings, three concurrent Forums were also held during the Summit.  A high level policy dialogue Forum was addressed by five permanent Secretaries from Commonwealth countries. The Technology and Innovation Forum was organized by University of Nottingham and the Haydn Green Foundation (UK).

A high level policy dialogue Forum was addressed by five permanent Secretaries from Commonwealth countries. The Technology and Innovation Forum was organized by University of Nottingham and the Haydn Green Foundation (UK). Participating senior policy makers and leaders of SME associations and Chambers from the Commonwealth countries discussed and agreed to create Framework of MSME Cooperation within the Commonwealth. Besides the Secretaries of Commerce and MSME, the senior officials from Government of India who chaired or coordinated different sessions included Additional Secretary Commerce Mr. Anup Wadhavan, Additional Secretary & Development Commissioner MSME Mr. S N Tripathi, Joint Secretary Commerce Mr. Damu Ravi and Director Commerce Mr. Bipin Menon.

Participating senior policy makers and leaders of SME associations and Chambers from the Commonwealth countries discussed and agreed to create Framework of MSME Cooperation within the Commonwealth. Besides the Secretaries of Commerce and MSME, the senior officials from Government of India who chaired or coordinated different sessions included Additional Secretary Commerce Mr. Anup Wadhavan, Additional Secretary & Development Commissioner MSME Mr. S N Tripathi, Joint Secretary Commerce Mr. Damu Ravi and Director Commerce Mr. Bipin Menon.

As entrepreneurs, we all follow our own path. For some, the rise to financial success is a long, slow, painful process. For others, things just seem to magically fall into place. I believe that the latter isn’t a result of magic, however, but is the sure sign of an entrepreneur who understands the importance of learning from, adapting to and growing with their business.

As entrepreneurs, we all follow our own path. For some, the rise to financial success is a long, slow, painful process. For others, things just seem to magically fall into place. I believe that the latter isn’t a result of magic, however, but is the sure sign of an entrepreneur who understands the importance of learning from, adapting to and growing with their business.

NEW DELHI: Chief Economic Adviser Arvind Subramanian today said the GDP growth is expected to further pick up by 0.75 per cent this fiscal on the back of policy support including macroeconomic measures. “Overall, my sense is that the economy could do with all the policy support it could to bring it back to full potential, especially, all the macroeconomic instruments that should be deployed to get the economy back to its full potential,” he said while reacting to subdued GDP number of 7.1 per cent for 2016-17.

NEW DELHI: Chief Economic Adviser Arvind Subramanian today said the GDP growth is expected to further pick up by 0.75 per cent this fiscal on the back of policy support including macroeconomic measures. “Overall, my sense is that the economy could do with all the policy support it could to bring it back to full potential, especially, all the macroeconomic instruments that should be deployed to get the economy back to its full potential,” he said while reacting to subdued GDP number of 7.1 per cent for 2016-17. Non-banking Finance Company (NBFC) Aye finance in a recent engagement with an International investment manager Blue Orchard, raised funds of 8 million dollars. These funds were raised through Non-Convertible Debentures with a maturity period of five years. Blue Orchard was formed under an initiative of the United Nations to manage microfinance debt investments worldwide. The company has extended funds of 8 million to Aye Finance.

Non-banking Finance Company (NBFC) Aye finance in a recent engagement with an International investment manager Blue Orchard, raised funds of 8 million dollars. These funds were raised through Non-Convertible Debentures with a maturity period of five years. Blue Orchard was formed under an initiative of the United Nations to manage microfinance debt investments worldwide. The company has extended funds of 8 million to Aye Finance. The Union Cabinet has given its nod to the ‘strategic partnership’ model under which select private firms will be roped in to build military platforms like fighter jets, submarines and battle tanks. The policy will give a boost to defence manufacturing by private defence majors including leading foreign firms. After the cabinet meeting, Defence Minister Arun Jaitley said the government wants to implement at the earliest the new model which is aimed at production of major defence platforms and equipment by Indian companies in collaboration with leading foreign firms.

The Union Cabinet has given its nod to the ‘strategic partnership’ model under which select private firms will be roped in to build military platforms like fighter jets, submarines and battle tanks. The policy will give a boost to defence manufacturing by private defence majors including leading foreign firms. After the cabinet meeting, Defence Minister Arun Jaitley said the government wants to implement at the earliest the new model which is aimed at production of major defence platforms and equipment by Indian companies in collaboration with leading foreign firms. With a little more than a month remaining for the implementation of the Goods and Services Tax (GST) in the country, the GST council has indicated that under the new tax regime there is huge scope for the Micro, Small and Medium Enterprises (MSMEs) to grow further. Arun Goyal, Additional Secretary of the GST council in a lecture at India International Center made these remarks. He further informed that over a period of time, the GST council is looking towards reducing the number of tax slabs. Currently under the GST bill, there is 5 per cent, 12 per cent, 18 per cent and 28 per cent tax slab; this might be reduced to 1 or 2 tax slabs.

With a little more than a month remaining for the implementation of the Goods and Services Tax (GST) in the country, the GST council has indicated that under the new tax regime there is huge scope for the Micro, Small and Medium Enterprises (MSMEs) to grow further. Arun Goyal, Additional Secretary of the GST council in a lecture at India International Center made these remarks. He further informed that over a period of time, the GST council is looking towards reducing the number of tax slabs. Currently under the GST bill, there is 5 per cent, 12 per cent, 18 per cent and 28 per cent tax slab; this might be reduced to 1 or 2 tax slabs. In a bid to help out Indian businesses floundering to comply with the Goods and Services Tax (GST), Ernst & Young (EY) has announced the launch of DigiGST – an integrated GSP-ASP (GST Suvidha Provider- Application Service Provider) solution that provides organisations with end-to-end GST compliance support. The company has hosted DigiGST on Microsoft Azure to ensure security to its clients. “The launch of GST is perhaps India’s most significant and complex economic reform and technology will play a critical role in this transformation journey.

In a bid to help out Indian businesses floundering to comply with the Goods and Services Tax (GST), Ernst & Young (EY) has announced the launch of DigiGST – an integrated GSP-ASP (GST Suvidha Provider- Application Service Provider) solution that provides organisations with end-to-end GST compliance support. The company has hosted DigiGST on Microsoft Azure to ensure security to its clients. “The launch of GST is perhaps India’s most significant and complex economic reform and technology will play a critical role in this transformation journey. With a view to provide timely financial support to MSMEs facing financial difficulties during their Life Cycle, RBI had advised the banks to review their existing lending policies and incorporating therein, among others, provisions for sanctioning of Standby Credit Facility in case of term loans, Additional Working Capital Limits, Mid Term Review of Regular Working Capital Limits, and Timelines for Credit Decisions, said SS Mundra, Deputy Governor, RBI.

With a view to provide timely financial support to MSMEs facing financial difficulties during their Life Cycle, RBI had advised the banks to review their existing lending policies and incorporating therein, among others, provisions for sanctioning of Standby Credit Facility in case of term loans, Additional Working Capital Limits, Mid Term Review of Regular Working Capital Limits, and Timelines for Credit Decisions, said SS Mundra, Deputy Governor, RBI. India’s 2017/18 sugar production will likely jump a quarter from the previous year to 25 million tonnes as decent monsoon rains are forecast, the head of an industry body told Reuters. That rebound in output to volumes near consumption levels could sap demand for imports from the world’s biggest consumer of the sweetener, dragging on international prices that are already near their lowest in over a year.

India’s 2017/18 sugar production will likely jump a quarter from the previous year to 25 million tonnes as decent monsoon rains are forecast, the head of an industry body told Reuters. That rebound in output to volumes near consumption levels could sap demand for imports from the world’s biggest consumer of the sweetener, dragging on international prices that are already near their lowest in over a year. Production of horticulture crops such as fruit and vegetables have seen an increase over the previous year. The production is estimated at 295 million tonnes in 2016-17 crop year ending June, shows the second advance estimates released by the agriculture ministry on Tuesday. Compared to the previous year when production was 286.18 million tonnes, the harvest is 3.1% higher. It is also 2.7% higher over the first advance estimate issued in February largely due to rise in on ..

Production of horticulture crops such as fruit and vegetables have seen an increase over the previous year. The production is estimated at 295 million tonnes in 2016-17 crop year ending June, shows the second advance estimates released by the agriculture ministry on Tuesday. Compared to the previous year when production was 286.18 million tonnes, the harvest is 3.1% higher. It is also 2.7% higher over the first advance estimate issued in February largely due to rise in on .. Urging the government to double the outlay of Rs 3,000 crore for development and management of fisheries sector, apex industry body Assocham on Tuesday said that India could achieve about 16 million metric tonnes (MMT) of inland and marine fisheries’ production by 2019-20 thereby adopting a target oriented approach to achieve eight per cent growth year-on-year. “Aided by government’s efforts to bring systemic changes in processing sector, the domestic segment in raw and processed fisheries sector in value terms is expected to touch Rs 1.5 lakh crore by 2020 and total domestic retail market is forecast to cross Rs 61 lakh crore or almost triple in next 4-5 years,” noted a just-concluded Assocham study titled ‘Fisheries in India: Potential & prospects; Reference state – West Bengal.’

Urging the government to double the outlay of Rs 3,000 crore for development and management of fisheries sector, apex industry body Assocham on Tuesday said that India could achieve about 16 million metric tonnes (MMT) of inland and marine fisheries’ production by 2019-20 thereby adopting a target oriented approach to achieve eight per cent growth year-on-year. “Aided by government’s efforts to bring systemic changes in processing sector, the domestic segment in raw and processed fisheries sector in value terms is expected to touch Rs 1.5 lakh crore by 2020 and total domestic retail market is forecast to cross Rs 61 lakh crore or almost triple in next 4-5 years,” noted a just-concluded Assocham study titled ‘Fisheries in India: Potential & prospects; Reference state – West Bengal.’ The Asian Development Bank (ADB) and the Punjab National Bank (PNB) have signed a USD 100 million loan to finance large solar rooftop systems on industrial and commercial buildings throughout India. The loan will be guaranteed by the Government of India. PNB will use the ADB funds to make further loans to various developers and end users to install rooftop solar systems. This is the first tranche loan of the USD 500 million multi tranche finance facility Solar Rooftop Investment Program (SRIP) approved by ADB in 2016.

The Asian Development Bank (ADB) and the Punjab National Bank (PNB) have signed a USD 100 million loan to finance large solar rooftop systems on industrial and commercial buildings throughout India. The loan will be guaranteed by the Government of India. PNB will use the ADB funds to make further loans to various developers and end users to install rooftop solar systems. This is the first tranche loan of the USD 500 million multi tranche finance facility Solar Rooftop Investment Program (SRIP) approved by ADB in 2016. West Bengal government has decided to utilise its unused land for setting up fruit farms. The project will start with a farm on 810 hectares unused piece of land, spread over Ranibandh, Raipur, Simlapal, Onda, Taldangra, Hirbandh and Indopur blocks of Bankura district. This is part of a mega project named as ’Horticulture Development in Paschimanchal Districts’. Five districts forming the western region of the state are part of this project – Bankura, Purulia, Paschim Medinipur, Birbhum and West Burdwan.

West Bengal government has decided to utilise its unused land for setting up fruit farms. The project will start with a farm on 810 hectares unused piece of land, spread over Ranibandh, Raipur, Simlapal, Onda, Taldangra, Hirbandh and Indopur blocks of Bankura district. This is part of a mega project named as ’Horticulture Development in Paschimanchal Districts’. Five districts forming the western region of the state are part of this project – Bankura, Purulia, Paschim Medinipur, Birbhum and West Burdwan. Odisha’s first Mega Food Park, M/s MITS Mega Food Park Pvt Ltd, has been inaugurated today by Harsimrat Kaur Badal, Minister of Food Processing Industries at Rayagada. The food park has facilities of fully operational industrial sheds for SMEs along with developed industrial plots for lease to food processing units. This is the 7th Mega Food Park operationalized in the last 3 years by the present government.

Odisha’s first Mega Food Park, M/s MITS Mega Food Park Pvt Ltd, has been inaugurated today by Harsimrat Kaur Badal, Minister of Food Processing Industries at Rayagada. The food park has facilities of fully operational industrial sheds for SMEs along with developed industrial plots for lease to food processing units. This is the 7th Mega Food Park operationalized in the last 3 years by the present government. The Haryana Government has invited the Union Minister for Micro, Medium and Small Enterprise (MSME) Kalraj Mishra for the scheduled MSME Sammelan on 30th of May in the state of Haryana. The MSME Sammelan is expected to be on the lines of innovation in the MSME sector. The Sammelan is likely to feature exhibition of various achievements and advancements by the industrial units in Haryana. The MSME Sammelan is being organized under the theme “Small is the new big”.

The Haryana Government has invited the Union Minister for Micro, Medium and Small Enterprise (MSME) Kalraj Mishra for the scheduled MSME Sammelan on 30th of May in the state of Haryana. The MSME Sammelan is expected to be on the lines of innovation in the MSME sector. The Sammelan is likely to feature exhibition of various achievements and advancements by the industrial units in Haryana. The MSME Sammelan is being organized under the theme “Small is the new big”. The Bankura district administration in West Bengal has received investment proposals worth Rs 600 crore at the received investment proposals worth Rs 600 crore. According to All India Trinamool Congress (AITC) around 305 investment proposals came from micro, small and medium enterprises (MSMEs) and the other proposals were from large industries. MSMEs like bakeries, rice mills, mechanised stone-crushing units, small-scale units manufacturing agricultural tools and roofing tiles, poultry fodder-making, agro-servicing units, sal-leaf cup-and-plate manufacturing, automobile painting and many others are successfully running their trade in the district.

The Bankura district administration in West Bengal has received investment proposals worth Rs 600 crore at the received investment proposals worth Rs 600 crore. According to All India Trinamool Congress (AITC) around 305 investment proposals came from micro, small and medium enterprises (MSMEs) and the other proposals were from large industries. MSMEs like bakeries, rice mills, mechanised stone-crushing units, small-scale units manufacturing agricultural tools and roofing tiles, poultry fodder-making, agro-servicing units, sal-leaf cup-and-plate manufacturing, automobile painting and many others are successfully running their trade in the district. The European country Belgium has recently expressed its interest to invest in the industries in the state of Uttarakhand. A delegation of Belgian trade counsellors led by Belgian Ambassador Jan Luykx recently met Chief Minister of Uttarakhand Trivendra Singh Rawat. During the talks the delegates have proposed investments in sectors including the herbal, food processing, aromatic plantation and spice sectors.

The European country Belgium has recently expressed its interest to invest in the industries in the state of Uttarakhand. A delegation of Belgian trade counsellors led by Belgian Ambassador Jan Luykx recently met Chief Minister of Uttarakhand Trivendra Singh Rawat. During the talks the delegates have proposed investments in sectors including the herbal, food processing, aromatic plantation and spice sectors.

During the 5th India Morocco Joint Commission Meeting (JCM) held in Rabat on 25 and 26 May 2017, both countries intensified the strong bilateral relations and provided an impetus for closer cooperation between the two countries in the political, commercial, cultural, and trade sectors. Nirmala Sitharaman, Commerce and Industry Minister gave keynote address at the Industry Day of Morocco in Casablanca, organised by the Ministry of Industry, Investment, Trade and Digital Economy of the Government of the Kingdom of Morocco.

During the 5th India Morocco Joint Commission Meeting (JCM) held in Rabat on 25 and 26 May 2017, both countries intensified the strong bilateral relations and provided an impetus for closer cooperation between the two countries in the political, commercial, cultural, and trade sectors. Nirmala Sitharaman, Commerce and Industry Minister gave keynote address at the Industry Day of Morocco in Casablanca, organised by the Ministry of Industry, Investment, Trade and Digital Economy of the Government of the Kingdom of Morocco.

After years of decline, Indian exports to China rose sharply in the first four months of this year registering a 20 per cent increase to $5.57 billion, though the trade deficit continued to persist. Indian exports received a major boost mainly due to China increasing the steel consumption by importing big quantity of iron ore as well as gems and diamonds besides cotton materials. The India-China trade grew by six per cent to $26.02 billion from January to April this year, according to the data of China’s customs accessed by PTI.

After years of decline, Indian exports to China rose sharply in the first four months of this year registering a 20 per cent increase to $5.57 billion, though the trade deficit continued to persist. Indian exports received a major boost mainly due to China increasing the steel consumption by importing big quantity of iron ore as well as gems and diamonds besides cotton materials. The India-China trade grew by six per cent to $26.02 billion from January to April this year, according to the data of China’s customs accessed by PTI. India and Africa can partner and their strong relations can be instrumental in shaping the future of the world, Finance Minister Arun Jaitley said at the inaugural of the 5 day Annual meeting of the 1st African Development bank summit in Gandhinagar. The Minister further said that the India-Africa partnership model provides huge scope as the inter-dependence is voluntary without any imposition and compulsions. The relations between the two nations have progressed to whole another level.

India and Africa can partner and their strong relations can be instrumental in shaping the future of the world, Finance Minister Arun Jaitley said at the inaugural of the 5 day Annual meeting of the 1st African Development bank summit in Gandhinagar. The Minister further said that the India-Africa partnership model provides huge scope as the inter-dependence is voluntary without any imposition and compulsions. The relations between the two nations have progressed to whole another level.

The 18th Session of India-Sweden Joint Commission for Economic, Industrial and Scientific Cooperation (JCEC) took place recently in the national capital. The discussion focussed on various themes including the cooperation between the two countries in the MSME sector Nirmala Sitharaman, Commerce and Industry Minister represented the Indian delegation at the JCEC and Ann Linde, Minister for Trade and EU Affairs and Foreign Affair Minister headed the Swedish delegation during the meet.

The 18th Session of India-Sweden Joint Commission for Economic, Industrial and Scientific Cooperation (JCEC) took place recently in the national capital. The discussion focussed on various themes including the cooperation between the two countries in the MSME sector Nirmala Sitharaman, Commerce and Industry Minister represented the Indian delegation at the JCEC and Ann Linde, Minister for Trade and EU Affairs and Foreign Affair Minister headed the Swedish delegation during the meet.

")

According to the FISME Factor, 100 percent of Micro, Small & Medium Enterprises (SMEs) are ready for GST.

According to the FISME Factor, 100 percent of Micro, Small & Medium Enterprises (SMEs) are ready for GST. The concept of human resource management (HRM) and human resource development (HRM/HRD) is an organized learning experience aimed at matching the organizational need for human resource (HR) with the individual need for career growth and development. It is a system and process involving organized series of learning the activities designed to produce behavioural changes in human beings in such a way that they acquire desired level of competence for present as well as future role.

The concept of human resource management (HRM) and human resource development (HRM/HRD) is an organized learning experience aimed at matching the organizational need for human resource (HR) with the individual need for career growth and development. It is a system and process involving organized series of learning the activities designed to produce behavioural changes in human beings in such a way that they acquire desired level of competence for present as well as future role. While the success of India’s demonetisation is being debated across both commercial and political corridors of power, there hasn’t been a better time for financial firms in the lending market. The surplus liquidity of cash in bank coffers has caused even banks to announce rate cuts on the loans provided.

While the success of India’s demonetisation is being debated across both commercial and political corridors of power, there hasn’t been a better time for financial firms in the lending market. The surplus liquidity of cash in bank coffers has caused even banks to announce rate cuts on the loans provided. Lead generation through effective B2B marketing is very important to stay competitive in the market. If you are not able to getting business leads through your marketing efforts, it means it will become problematic for your business as no revenue will come sooner or later.You may be familiar about how difficult it has been to market your services and products by using available sources smartly.

Lead generation through effective B2B marketing is very important to stay competitive in the market. If you are not able to getting business leads through your marketing efforts, it means it will become problematic for your business as no revenue will come sooner or later.You may be familiar about how difficult it has been to market your services and products by using available sources smartly. TThe North East Industrial and Investment Promotion Policy (NEIIPP) which was revoked have caused a great loss to the industrial growth in the North Eastern States. While there have been talks of brining a new policy, the industry says with no policy in place, the state is already suffering.

TThe North East Industrial and Investment Promotion Policy (NEIIPP) which was revoked have caused a great loss to the industrial growth in the North Eastern States. While there have been talks of brining a new policy, the industry says with no policy in place, the state is already suffering. Saving and investing can be a daunting task for most. But what if you could save effortlessly, like while watching your favourite football team win or walking those 10,000 steps a day? For IIT Kanpur alumni Ankit Kumar and Abhishek Malik, the answer to that question was a startup, though it wasn’t their first. While Ankit holds a master’s degree in design, Abhishek graduated with a degree in economics.

Saving and investing can be a daunting task for most. But what if you could save effortlessly, like while watching your favourite football team win or walking those 10,000 steps a day? For IIT Kanpur alumni Ankit Kumar and Abhishek Malik, the answer to that question was a startup, though it wasn’t their first. While Ankit holds a master’s degree in design, Abhishek graduated with a degree in economics. Every day for the past few years, Gyan Kesarwani kept one foot in the past, deriving an insatiable drive from the financially trying times he encountered. With his other foot in the future, he was innovating swiftly to usher in the next generation of technology, while keeping his day job as an educator for budding techies.

Every day for the past few years, Gyan Kesarwani kept one foot in the past, deriving an insatiable drive from the financially trying times he encountered. With his other foot in the future, he was innovating swiftly to usher in the next generation of technology, while keeping his day job as an educator for budding techies. “ Non-violence leads to the highest ethics, which is the goal of all evolution. Until we stop harming all other living beings, we are still savages. ”

“ Non-violence leads to the highest ethics, which is the goal of all evolution. Until we stop harming all other living beings, we are still savages. ”